Data Through Q1 2024

Introduction: The CoreLogic Homeowner Equity Insights report, is published quarterly with coverage at the national, state and metro level and includes negative equity share and average equity gains. The report features an interactive view of the data using digital maps to examine CoreLogic homeowner equity analysis through the first quarter of 2024.

Negative equity, often referred to as being “underwater” or “upside down,” applies to borrowers who owe more on their mortgages than their homes are worth. Negative equity can occur because of a decline in home value, an increase in mortgage debt or both.

This data only includes properties with a mortgage. Non-mortgaged properties (that are owned outright) are not included.

Homeowner Equity Q1 2024: CoreLogic analysis shows U.S. homeowners with mortgages (roughly 62% of all properties*) have seen their equity increase by a total of $1.5 trillion since the first quarter of 2023, a gain of 9.6% year over year.

*Homeownership mortgage source: 2016 American Community Survey.

Chart 1: U.S. home equity changes year over year, Q1 2024In the first quarter of 2024, the total number of mortgaged residential properties with negative equity decreased by 2.1% from the fourth quarter of 2023, representing 1 million homes, or 1.8% of all mortgaged properties. On a year-over-year basis, negative equity declined by 16.1% from 1.2 million homes, or 2.1% of all mortgaged properties, from the first quarter of 2023.

Because home equity is affected by home price changes, borrowers with equity positions near (+/- 5%) the negative equity cutoff are most likely to move out of or into negative equity as prices change, respectively. Looking at the first quarter of 2024 book of mortgages, if home prices increase by 5%, 110.000 homes would regain equity; if home prices decline by 5% 153,000 would fall underwater. The CoreLogic HPI Forecast TM projects that home prices will increase by 3.7% from March 2024 to March 2025.

Chart 2: U.S. negative home equity changes year over year, Q1 2024California Leads U.S. for Annual Equity Gains in Q1

U.S. homeowners with a mortgage continued to see healthy annual equity gains in the opening quarter of 2024. As one of the nation’s most expensive states with perpetually high housing demand, California homeowners saw the largest equity gain in the country at $64,000, with those in the Los Angeles metro area netting $72,000 year over year. Most of the other large equity gains were concentrated in the Northeast, including New Jersey ($59,000), a state that has ranked in the top three for annual appreciation in CoreLogic’s monthly Home Price Insights report since last fall.

National Aggregate Value of Negative Equity: Q1 2024

The national aggregate value of negative equity was approximately $321 billion at the end of the first quarter of 2024. This is down quarter over quarter by approximately $2.8 billion, or 1%, from $324 billion in the fourth quarter of 2023 and down year over year by approximately $17.6 billion, or 5%, from $339 billion in the first quarter of 2023.

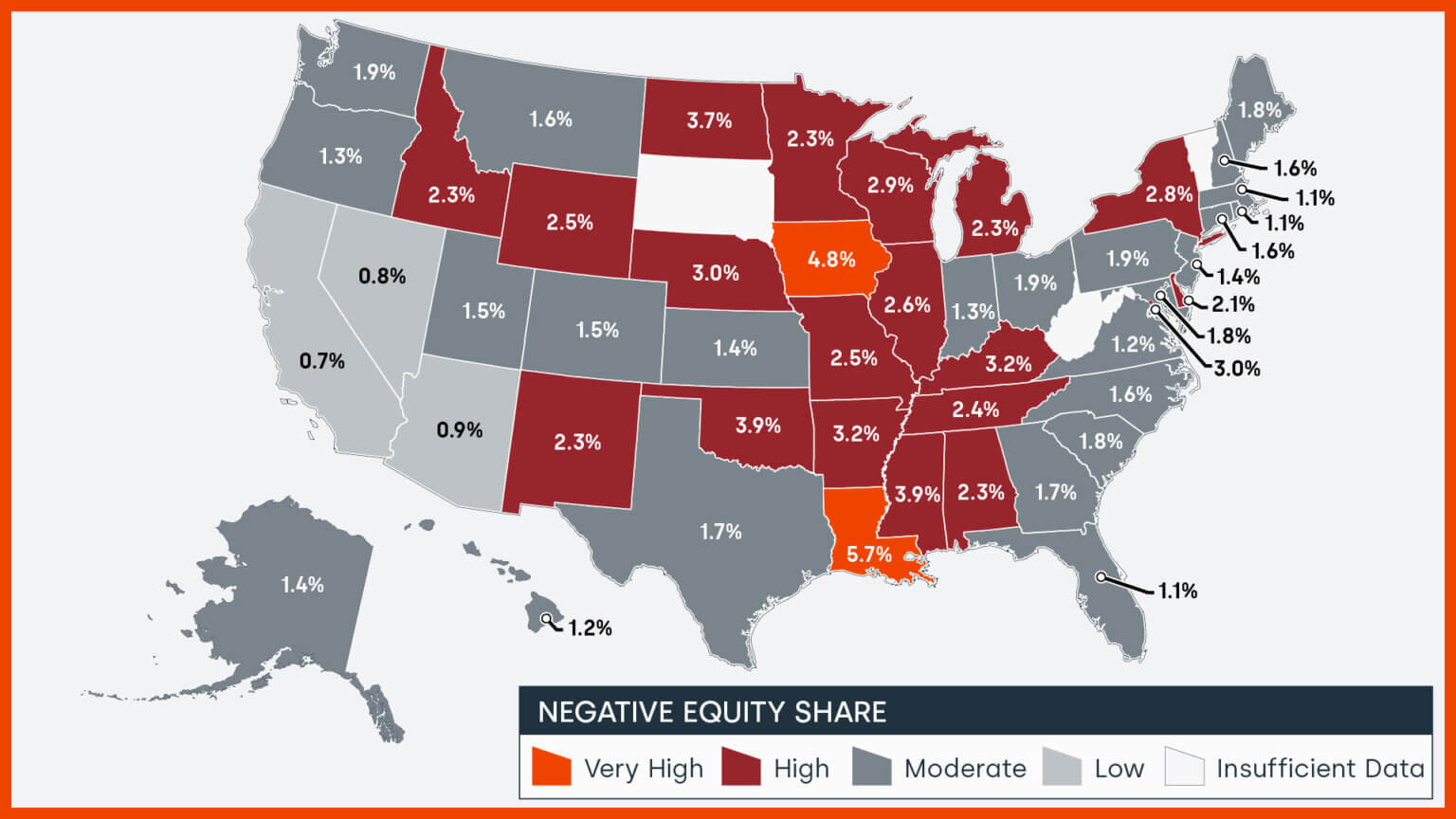

Negative equity peaked at 26% of mortgaged residential properties in the fourth quarter of 2009, based on the CoreLogic equity data analysis which began in the third quarter of 2009.

Chart 3: Negative equity share by U.S. state, Q1 2024“With home prices continuing to reach new highs, owners are also seeing their equity approach the historic peaks of 2023, close to a total of $305,000 per owner. Importantly, higher prices have also lifted some 190,000 homeowners out of negative equity, leaving only about 1.8% of those with mortgages underwater. Home equity is key to mortgage holders who have seen other homeownership costs soar, including insurance, taxes and HOA fees, as a source of financial buffer. Also, low amounts of negative equity are welcomed in markets that have shown price weaknesses this spring, such as Florida (1.1% of homes underwater) and Texas (1.7% of homes underwater) — both of which are below the national rate — as further price declines could drive more homeowners to lose their equity.”

-Dr. Selma Hepp

Chief Economist for CoreLogic

National Homeowner Equity

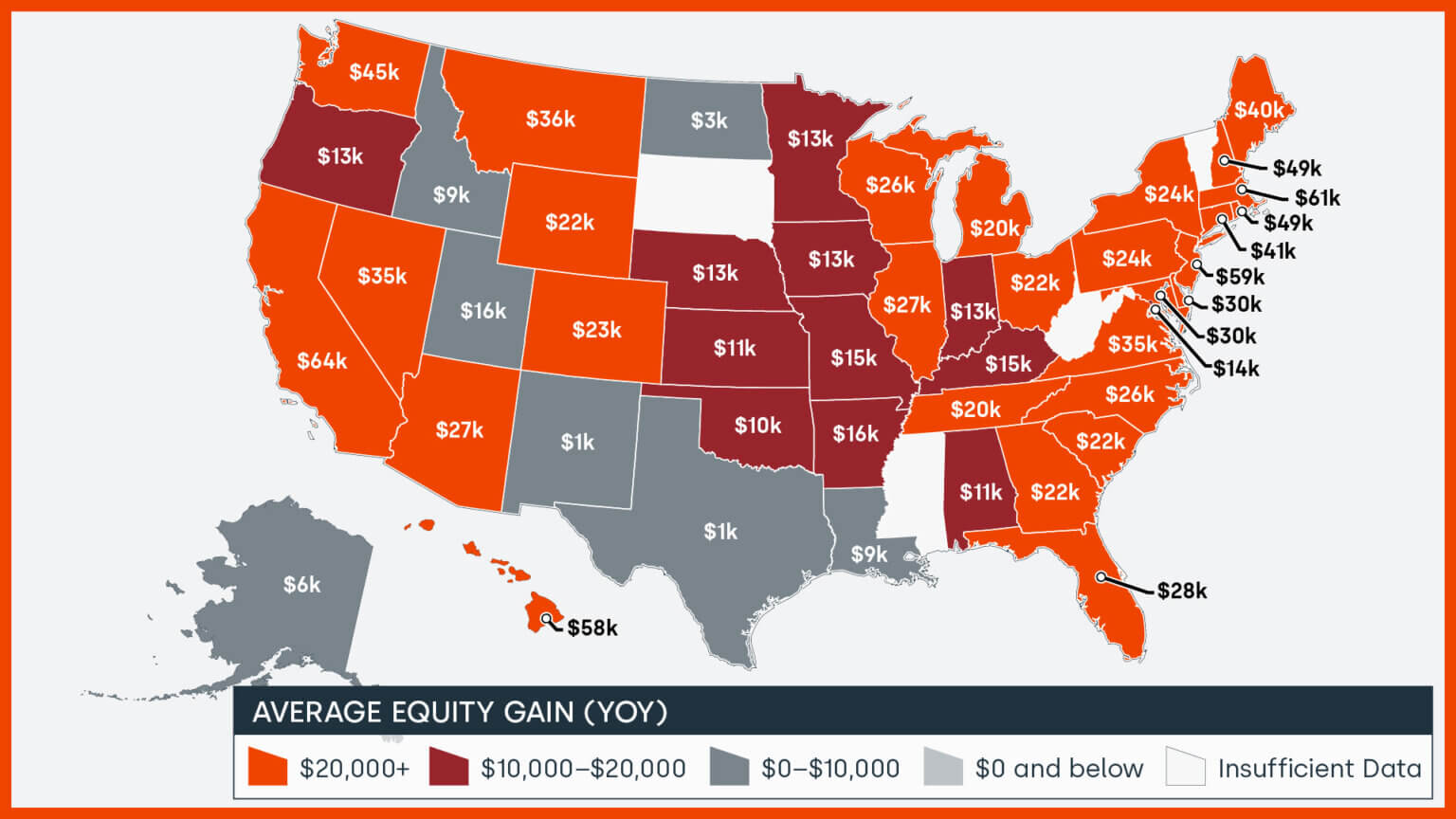

In the first quarter of 2024, the average U.S. homeowner gained approximately $28,000 in equity during the past year.

California ($64,000), Massachusetts ($61,000) and New Jersey ($59,000) posted the largest average national equity gains. No states saw annual equity losses.

Chart 4: Average home equity changes by U.S. state year over year, Q1 202410 Select Metros Change

CoreLogic provides homeowner equity data at the metropolitan level, in this graphic 10 of the largest cities, by housing stock are depicted.

Negative equity has seen a recent decrease across the country. Las Vegas is the least challenged, with the negative equity share of all mortgages at 0.6%.

Chart 5: Percentage of homes in negative equity for 10 select U.S. metro areas, Q1 2024Loan-to-Value Ratio (LTV)

This chart shows National Homeowner Equity Distribution across multiple LTV Segments.

Chart 6: Home equity distribution across multiple LTV segments, Q4 2023 and Q1 2024

Summary

CoreLogic began reporting homeowner equity data in the first quarter of 2010; at that time, the equity picture for homeowners was rather bleak in the United States. Since then, many homes have regained equity and the outstanding balance on the majority of mortgages in this country are now equal to or in a positive position when compared to their loan balance.

CoreLogic will continue to report on homeowner equity as it continues to adjust in communities and states across the country. To learn more about homeowner equity, visit the CoreLogic Intelligence home page.

Methodology

The amount of equity for each property is determined by comparing the estimated current value of the property against the mortgage debt outstanding (MDO). If the MDO is greater than the estimated value, then the property is determined to be in a negative equity position. If the estimated value is greater than the MDO, then the property is determined to be in a positive equity position. The data is first generated at the property level and aggregated to higher levels of geography. CoreLogic uses public record data as the source of the MDO, which includes more than 50 million first- and second-mortgage liens, and is adjusted for amortization and home equity utilization in order to capture the true level of MDO for each property. Only data for mortgaged residential properties that have a current estimated value are included. There are several states or jurisdictions where the public record, current value or mortgage data coverage is thin and have been excluded from the analysis. These instances account for fewer than 5% of the total U.S. population. The percentage of homeowners with a mortgage is from the 2019 American Community Survey. Data for the previous quarter was revised. Revisions with public records data are standard, and to ensure accuracy, CoreLogic incorporates the newly released public data to provide updated results.

CoreLogic HPI Forecasts™ are based on a two-stage, error-correction econometric model that combines the equilibrium home price—as a function of real disposable income per capita—with short-run fluctuations caused by market momentum, mean-reversion, and exogenous economic shocks like changes in the unemployment rate. With a 30-year forecast horizon, CoreLogic HPI Forecasts project CoreLogic HPI levels for two tiers — “Single-Family Combined” (both attached and detached) and “Single-Family Combined Excluding Distressed Sales.” As a companion to the CoreLogic HPI Forecasts, Stress-Testing Scenarios align with Comprehensive Capital Analysis and Review (CCAR) national scenarios to project five years of home prices under baseline, adverse and severely adverse scenarios at state, metropolitan areas and ZIP Code levels. The forecast accuracy represents a 95% statistical confidence interval with a +/- 2% margin of error for the index.

Source: The data provided is for use only by the primary recipient or the primary recipient’s publication or broadcast. This data may not be re-sold, republished or licensed to any other source, including publications and sources owned by the primary recipient’s parent company without prior written permission from CoreLogic. Any CoreLogic data used for publication or broadcast, in whole or in part, must be sourced as coming from CoreLogic, a data and analytics company. For use with broadcast or web content, the citation must directly accompany first reference of the data. If the data is illustrated with maps, charts, graphs or other visual elements, the CoreLogic logo must be included on screen or website. For questions, analysis or interpretation of the data, contact Robin Wachner at newsmedia@corelogic.com. For sales inquiries, please visit https://www.corelogic.com/support/sales-contact/. Data provided may not be modified without the prior written permission of CoreLogic. Do not use the data in any unlawful manner. This data is compiled from public records, contributory databases and proprietary analytics, and its accuracy is dependent upon these sources.

About CoreLogic: CoreLogic is a leading provider of property insights and innovative solutions, working to transform the property industry by putting people first. Using its network, scale, connectivity and technology, CoreLogic delivers faster, smarter, more human-centered experiences that build better relationships, strengthen businesses and ultimately create a more resilient society. For more information, please visit www.corelogic.com.

Original Post